The flags of NATO’s member-states outside its Brussels headquarters (Source: NATO through CC BY-NC-ND 2.0)

Europe is dealing with a changing security environment. The war in Ukraine has brought conflict back to its doorstep for the first time since World War 2. The American security guarantee that ensured peace in the continent is not considered as ironclad as it once was due to the increasing polarisation of American commitments overseas and increasing competition in the Indo-Pacific. Recognising their outsized dependence on the U.S. for their security and the various increasing external threats, European states have begun increasing their own capabilities to prepare for a more European NATO.

Dependence on the United States

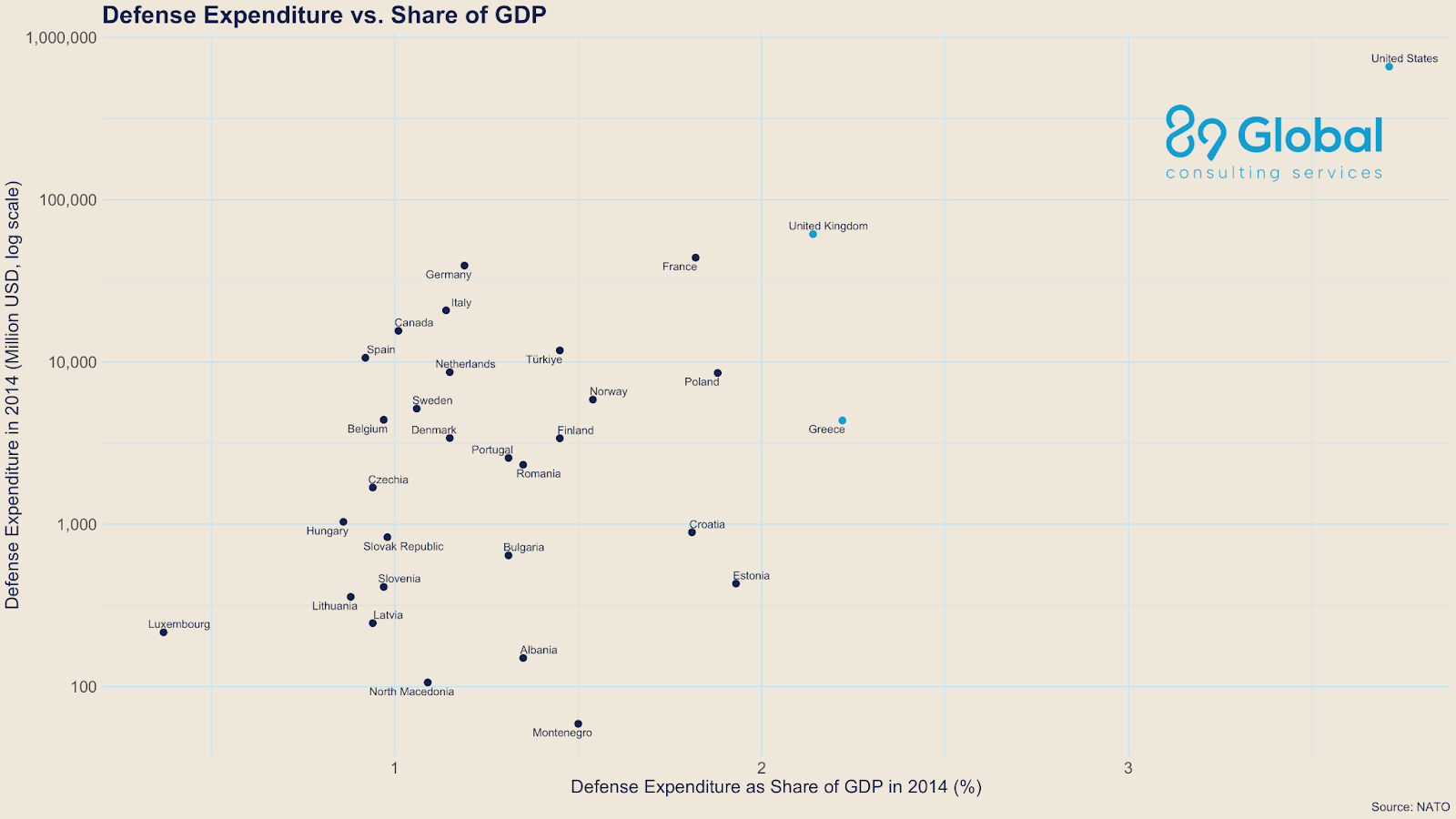

The United States is by far the largest contributor to NATO. It spent more than $860 billion on defence last year, roughly 3.5% of its GDP. Its defence expenditure accounted for more than 68% of the total defence expenditure of NATO member states in 2023. Spending 10 times more than Germany, the NATO member state with the second-largest defence expenditure, the United States contributes a significant portion of its defence expenditure on European defence. In 2014, only three NATO member states spent more than 2% of their GDP on defence.

Given the intensifying security competition with China in the Indo-Pacific, the U.S. fears that it might get overextended in Europe to the advantage of China, which is perceived as the bigger direct threat. To that end, American presidents since President Obama have urged other NATO member states to pick up the slack and spend at least 2% of their GDP on defence. Among Trump’s supporters, however, there are also proposals to restructure the security architecture of the alliance by having the United States relegate itself to a support role and hand over European combat responsibility to the European nations.

The European Response

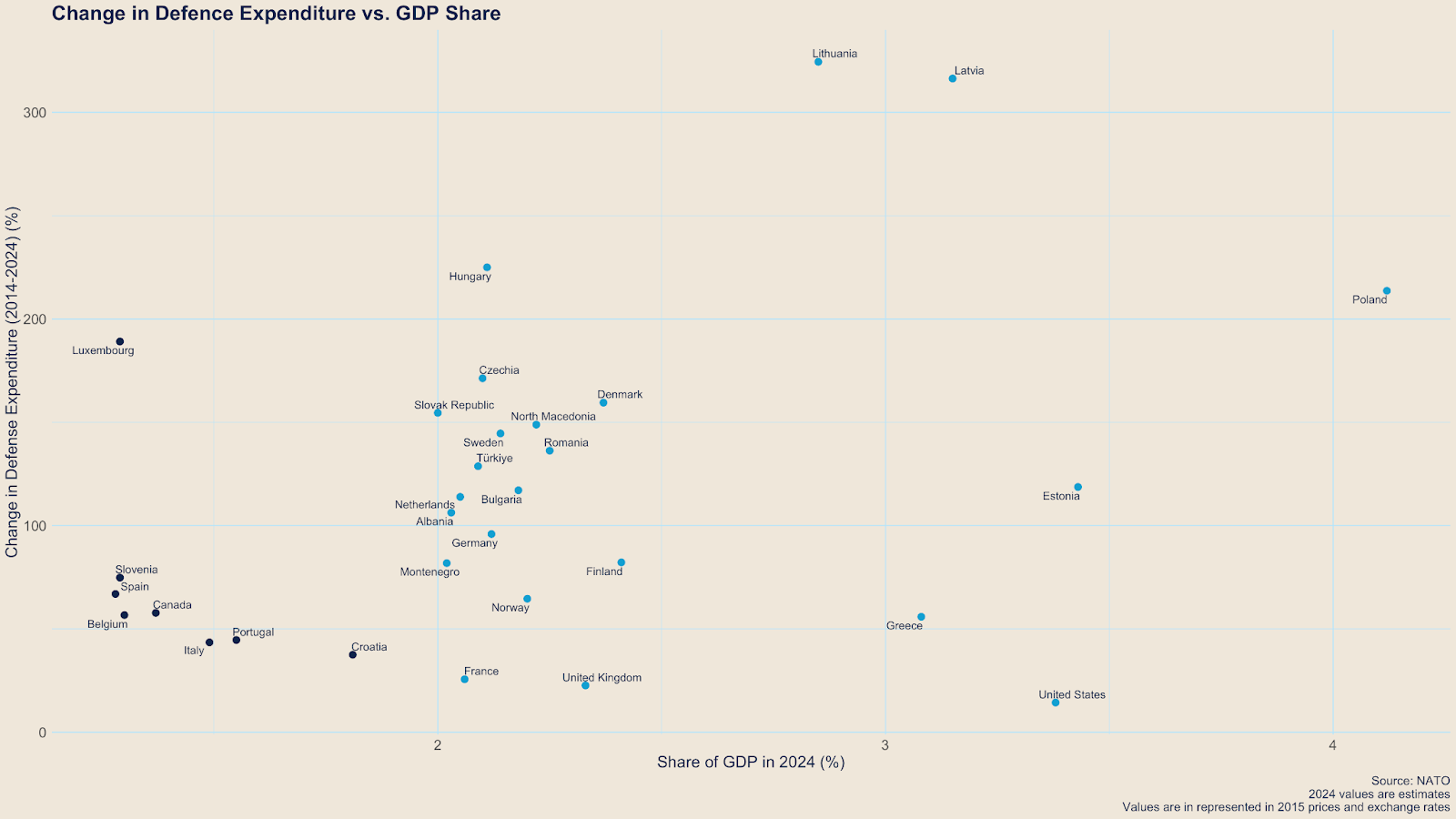

There has been increasing consensus among European leaders about the need to assume greater responsibility for their defence. The war in Ukraine has brought Europe’s underspending in defence into sharp focus. European states have made progress in increasing their defence expenditures over the last decade. In July, at the heels of the NATO summit, Secretary General Jens Stoltenberg announced that 23 member states will now meet the 2% mark for defence expenditure. European NATO members now constitute 34% of NATO’S military spending. Poland and the United Kingdom have called for NATO member states to spend more than 2% of their GDP on defence whereas the German Defence Minister, Boris Pistorius, has urged his country to spend up to 3.5% of its GDP on defence. German armed forces are beginning their first permanent foreign deployment in Lithuania, demonstrating an initiative to take on greater combat responsibility in NATO.

The European Council’s Strategic Agenda for 2024-29 envisions “a strong and secure Europe” through increased investment in defence, the creation of a better integrated European defence market, enhanced interoperability between European armed forces, and promotion of joint procurement. It also underlines the economic basis of collective European security, calls for flagship projects and defence initiatives by member states, and promises to increase access to public and private finance through all options, including enhancing the role of the European Investment Bank Group.

European private investment in defence has also been on the rise, partially due to concerns over a reorientation of American foreign policy towards Europe after the impending American elections. Local defence technology startups have demonstrated relative resilience amid a downturn in venture capital (VC) funding in 2023. Furthermore, VCs such as the €1 billion NATO Innovation Fund (NIF), backed by 24 NATO member states, are actively involved in investing in defence startups to increase European security. NIF recently entered into a partnership with the European Investment Fund (EIF), a part of the European Investment Bank, to support the growth of defence and security industries across Europe.

The EU’s first-ever European Defence Industrial Strategy (EDIS), unveiled earlier this year, aims to bolster the European defence sector by laying out several targets for EU member states. Given that currently 78% of European defence acquisitions come from outside the EU, it encourages member states to buy at least 40% of their defence equipment through collaboration. It also recommends that 50% of their defence procurement budgets be spent on products made within Europe and at least 35% of defence trade to occur within the EU instead of with external partners. The European Commission has proposed the European Defence Industry Programme, a regulation that seeks to implement the proposals outlined in the EDIS and provide €1.5 billion in financial support to the European Defence Industry. The Draghi Report on the future of European competitiveness particularly highlights the fragmented nature of the European defence industry and its lack of innovation and calls for greater cohesiveness and research and development at the European level.

Challenges

Although Europe has begun undertaking efforts to increase its sufficiency in defence and security, considerable challenges still remain. Decades of underinvestment in defence would need time to be rectified and for their effects to become visible. Furthermore, European defence expenditure and investment is still lagging. For example, EDIP’s €1.5 billion is dwarfed by the larger pool of European expenditure, making it difficult for it to have much impact. Germany’s attempts at ramping up its defence expenditure have run into financial constraints.

Operationally, the U.S. is much better equipped, and largely responsible for support roles such as reconnaissance, aerial refuelling, and satellite communications. Washington is viewed as the leader and organiser of the alliance, as was clearly visible during the 2022 Russian invasion. Increased NATO-EU engagement is also necessary to ensure that EU programmes are aligned with defence planning priorities at the national level and at NATO.

Implications for Governments

- NATO’s European members can reduce their outsized dependence on the United States for their security. With growing consensus among Europe’s leaders, there is political momentum for states to undertake initiatives to increase their responsibilities within NATO.

- While defence expenditures have largely been increasing across Europe, European defence commitments have been meeting strategic constraints. This might undermine European hopes of increasing their self-sufficiency in security.

- The U.S. can expect European demand for its defence exports to drop as Europe seeks to build its own defence industrial base.

- Increasing defence expenditures could have costs such as increasing taxes, etc.

Implications for Firms

- European firms in the strategic sectors of defence and security have the opportunity to take advantage of the increased opportunities created by renewed calls for countries to procure from within Europe.

- European firms have greater incentives to collaborate on the production of defence goods.

- Firms are likely also to experience increased access to private financing options.