The trade of Eurasia, the great land mass connecting Europe and Asia, was once said to ‘spin’ on Turkey. For centuries, this country formed a thoroughfare for the world’s most valued goods. Silks, spices, sugars, tobacco, and powerful narcotics criss-crossed along its dusty camel-laden routes, uniting worlds seemingly far apart.

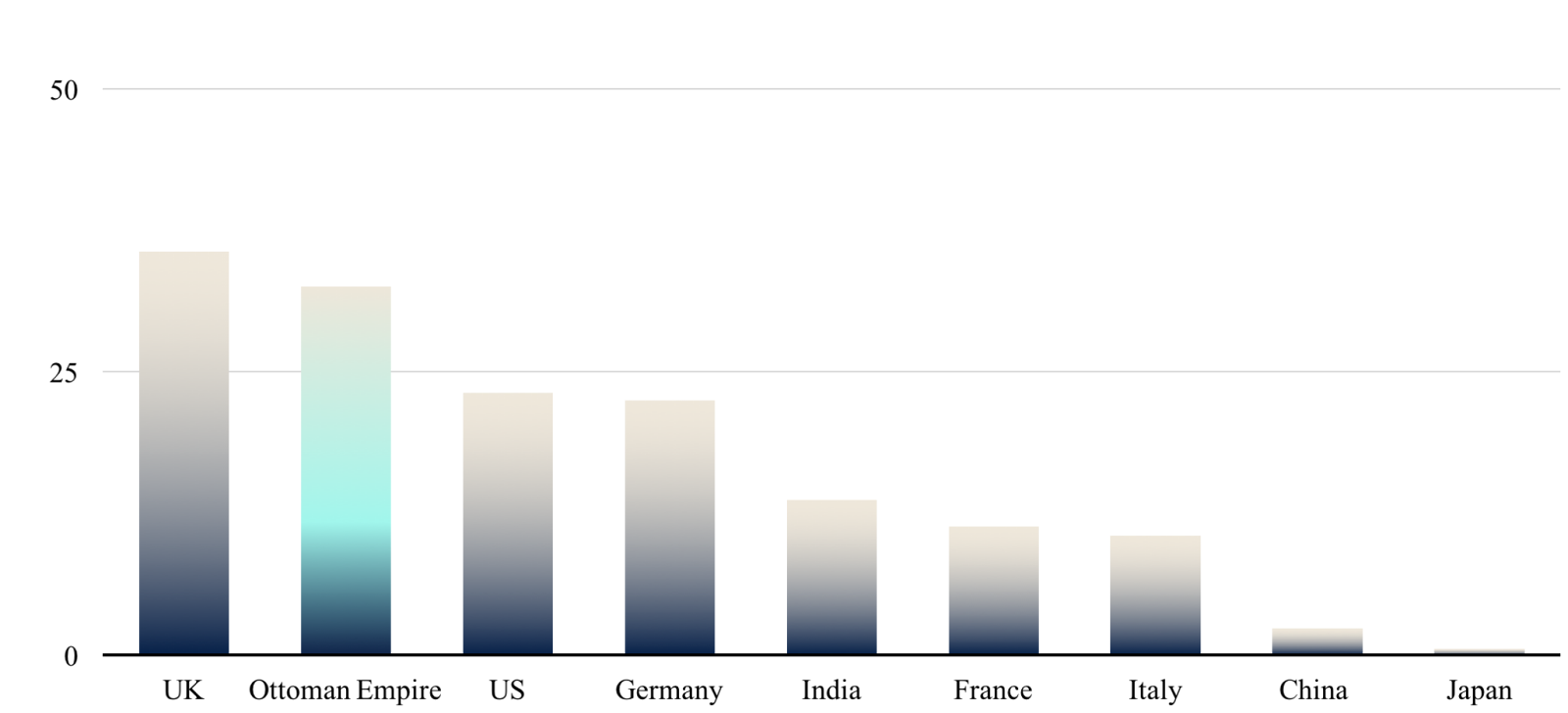

During the Ottoman Empire, the region played an important role in world trade. Partly, this was due to the demand for its own goods – raisins, the veritable ‘sultanas’, cotton, and opium were cultivated en masse in western Anatolia. But this role stemmed in great part from the unique position of the region as a connector of goods and people. Indeed, it was from the transit of commodities and goods that the Ottoman Empire derived much of its importance to world trade. Over 30% of exports throughout the last century of the Ottoman Empire consisted in the re-sale of goods previously imported from outside. Principally, such goods would be imported from the Middle East or India, before their export to the great centres of Europe. In the late 19th century, this made Turkey one of the world’s most important sites for the trans-shipment and trans-loading of foreign goods (See Exhibit 1).

Exhibit 1: Percentage of exports deriving from trans-shipment or trans-loading (1890)

Trans-shipment involves the unloading of goods from one ship to another; trans-loading, the switching from maritime to road transport, or vice versa. These methods have long been used to slash trading costs, promote speed, and avoid border and customs restrictions. During the Late

Ottoman Empire, foreign goods would be brought by local middlemen through the Suez Canal from India, or by land from Iran. They would be stored for safety and preservation in one of the many thousand caravanserais, before wending their way westward. Port cities like Istanbul and Izmir were the natural termini, where goods were loaded on ships, before chugging onwards to the great metropolises of Europe.

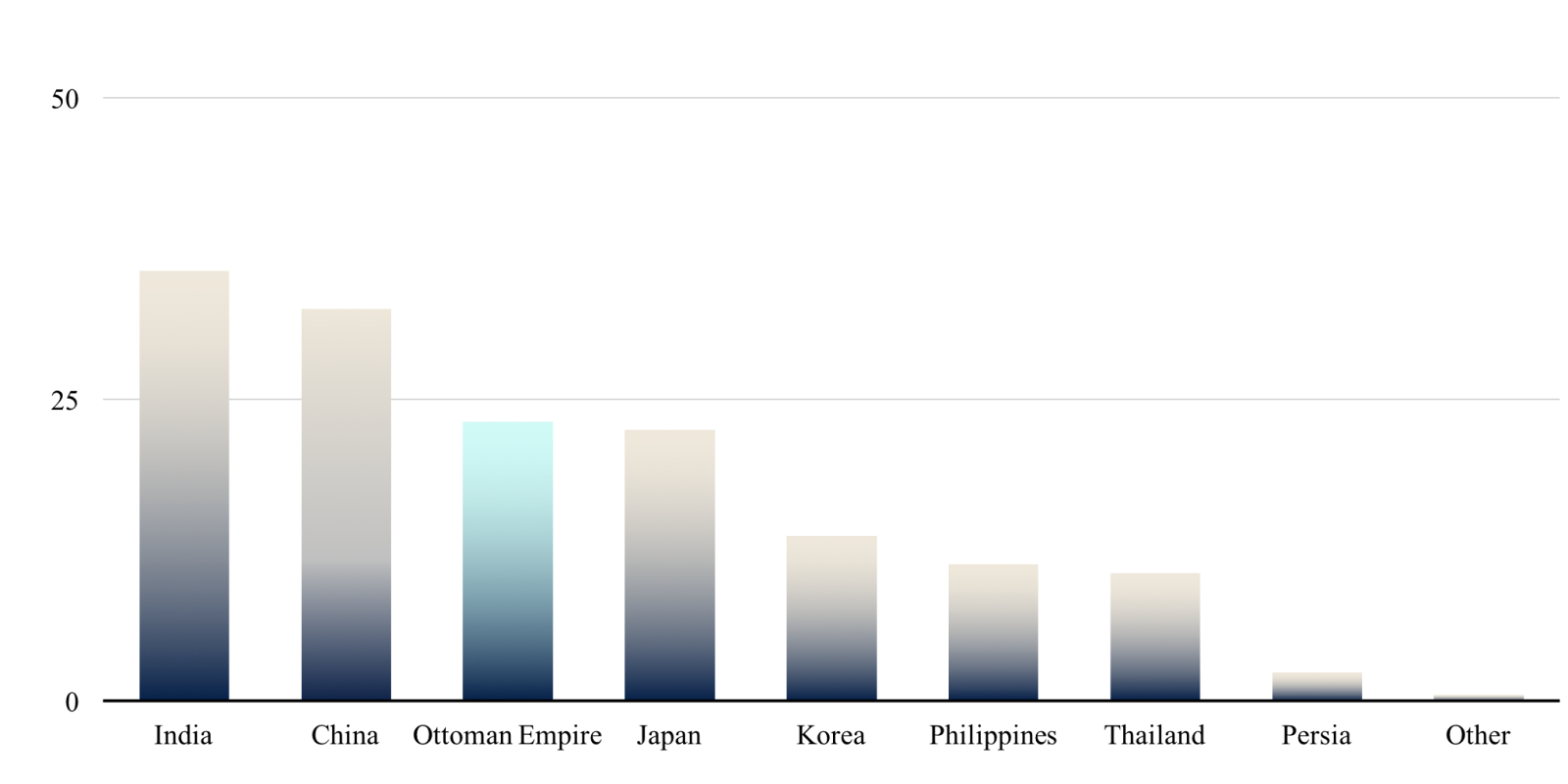

The role of Anatolia as a transit hub allowed the Ottoman Empire to remain relevant to world trade, even as its political power was on the wane. Between 1800-1890, the Ottoman Empire’s share of global exports stayed above 1.5%, while its proportion of Asian exports remained steady at roughly 8.5%, behind India and China, but ahead of Japan, Korea, Persia, Thailand, and the Philippines. Figure 2 demonstrates this pattern.

Exhibit 2: Percentage of all exports from Asia (1830-1890)

However, after the collapse of the Ottoman Empire the importance of Turkey as a global trade hub declined precipitously. By 1965, its share of global exports had declined to 0.23%. By 1980, it remained low at 0.44%, while its share of exports from Asia also declined. The growth of the large East Asian economies is likely to account for a portion of this effect. However, the economic policies of modern Turkey also played a crucial role.

The statist approach of early Turkish governments to the economy, which for decades sought to muzzle imports to promote national industry, limited the potential of Turkey to recreate its earlier role as a transit hub. Data analysed by 89 Global shows the impact that trade-substituting policies of the early Turkish Republic had on its relative share of global exports, and on the share of total exports from the Asian continent.

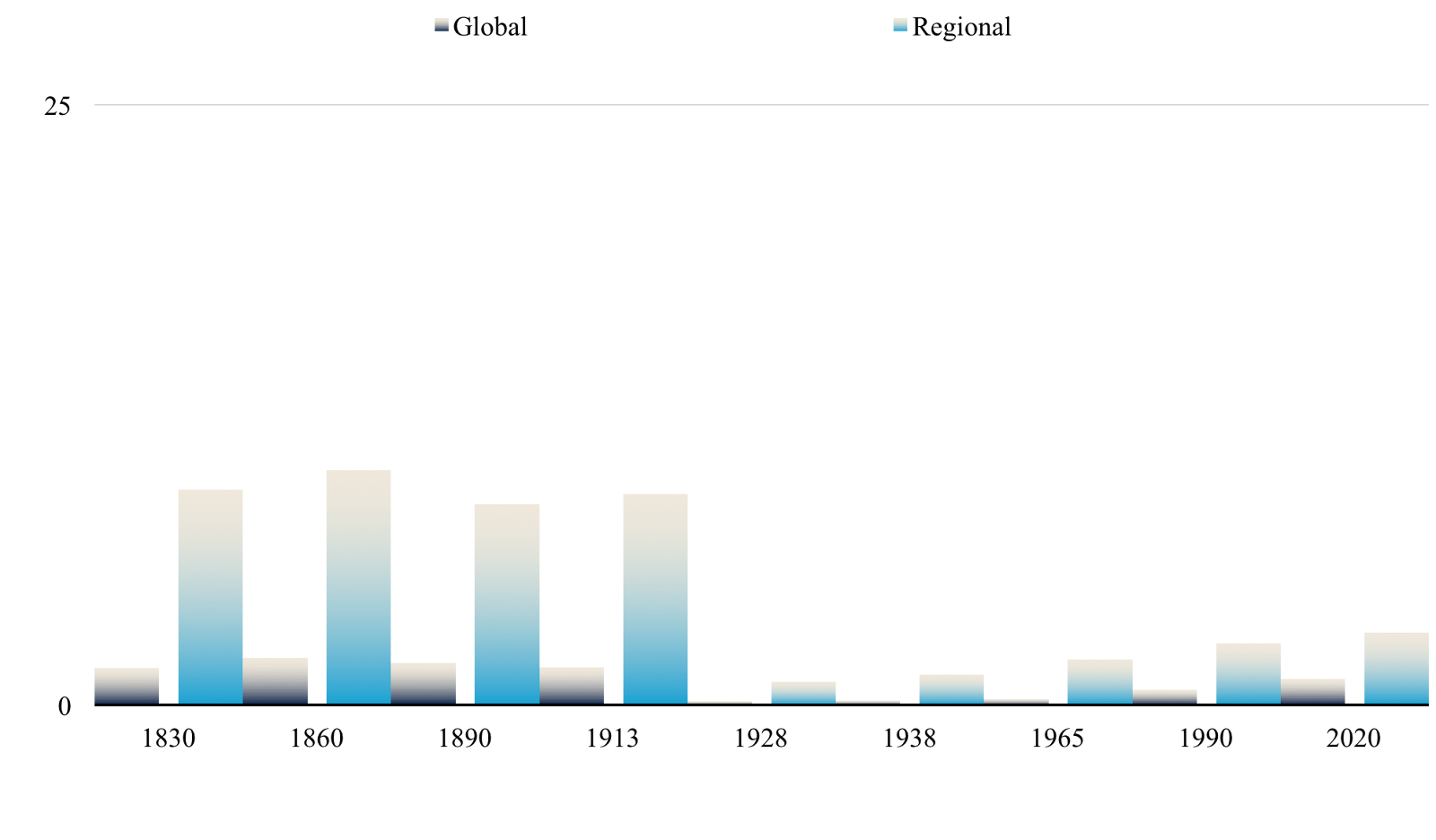

The constraints placed on imports are strongly correlated with a reduction in the global share of exports. By reducing imports, early Turkish governments ended the country’s role as a transit hub. Without a vibrant import economy, Turkey lost its crucial trans-shipment and trans-loading trade and, by consequence, suffered a considerable reduction in exports. Figure 3 below demonstrates Turkey’s shrinking proportion of global exports, and its share among Asian exports, since the last days of the Ottoman Empire.

Exhibit 3: Turkey: share of exports (global and regional)

Re-emergence as a transit hub

However, important reforms in the 1980s helped to liberalise imports and re-orient the country towards international commerce. The 1995 Customs Union agreement with the EU, Turkey’s biggest trading partner, presaged a significant uptick in European imports. The re-vitalisation of imports helped the Turkish economy grow with renewed zeal, something which has seen Turkey emerge as a regional economic power in the last two decades. It has also coincided with an uptick in exports, which have almost doubled as a relative global share between 1990-2020. While the economy has been experiencing a major foreign exchange and inflation crisis in recent years, and while its human rights record is under scrutiny, its position in global trade continues to grow in importance.

Several specific factors underlie the galloping growth in exports. Foreign direct investment and a booming industry for cheap electrical appliances have been important in this regard. But these trends pale in comparison with the impact felt by the great reopening to imports. Crucially, this has seen Turkey re-emerge as a trans-shipment and trans-loading hub. Goods arriving from Russia, China, the Middle East, Africa, and the Balkans are often sold on to markets further afield.

In 2013, the European Bank for Reconstruction and Development (EBRD) invested in Turkey’s first trans-shipment container terminal, AsyaPort in Tekirdag province. Vessels capable of carrying more than 6,500 TEUs cannot traverse the Bosporus straits, which connects the Mediterranean with the Black Sea. Thus, AsyaPort receives cargos from larger ships in the Marmara Sea, before being picked up by smaller vessels for the journey through the straits. In recent years, the straits have become critical to the grain supply for countries of the Global South. Today, grain-rich Russia and Ukraine account for 20% of global grain exports, roughly 40% of which pass via trans-shipment through Turkey, mainly through AsyaPort.

Several smaller trans-shipment centres have also been established, serving routes connecting Europe with central Asia, and the Indian Ocean. The Gemlik facility, also on the Marmara Sea, principally serves the central Asian route, linking with the Caucasus entrepots of Baku and Astrakhan, as part of the International North-South Transport Corridor. This route connects Europe with East Asia, and is crucial for the movement of rare earth metals (REMs) and critical raw materials (CRMs). Millions of tonnes of REMs and CRMs, originating in China, Myanmar, and Thailand are shipped annually across the Indian Ocean, passing via Turkey to the EU, which is almost entirely reliant on CRMs from outside.

The resurgence of Turkey as a trans-shipment hub also presages the revival of several port cities dotting the Anatolian coastline, each formerly crucial to the transit economy of the Late Ottoman Empire. Most notably, the port of Izmir is re-discovering its historical role as a major transport and logistics hub for the wider region. Its trans-shipment facilities at Bayraklı are the second largest in Turkey, after AsyaPort, serving 4,500 import firms and a similar number of export firms. Large trans-shipment and trans-loading hubs have also been established in Adana, Mersin, and Iskenderun, to cater to the growing demand.

The geopolitics of the transit economy

Amidst this revival, regional geopolitics force Turkey increasingly to reconcile the growing importance of trans-shipment and trans-loading to its economy, with the diplomatic exigencies of its wider strategic position. Situated between major geopolitical zones – the EU, Russia, the Middle East, and the Eastern Mediterranean – the country forms a natural commercial and diplomatic bridge. Given the geopolitical importance of Turkey, its strategic and military interventions can prove catalytic in the wider diplomatic arena. To manage the sensitivity of its position, Turkish governments have tended to avoid choosing sides, opting to retain close ties with all regional players in the neighbourhood.

These dynamics have implications for the transit economy. During the Russo-Ukrainian War, Turkey has refused to follow the western policy on Russian sanctions, continuing to trade freely with Russia throughout. As such, it has been used by certain firms as a means of circumventing prohibitions on the entry of Russian goods to the EU. The method for this is relatively simple. EU-based companies use middlemen, in Turkey, or in other centres such as Dubai, which act as entrepots, to purchase Russian goods. The goods are then sold on to the EU. While this mechanism is not illegal, EU officials argue that the system is blunting the effectiveness of sanctions.

Yet the continued reliance of the EU on raw materials from Russia means it has thus far desisted from taking a firmer stance. The EU remains dependent on Russian copper, which it has continued to import using the middleman method, mainly through Asya Port. This reality means that Turkey’s role in this commercial-diplomatic web is unlikely to be compromised in the near future.

Outlook

The growing importance of Turkey as an energy hub, in the wake of the Russo-Ukrainian War, will likely accelerate the expansion of its transit economy. It has been proposed that the planned natural gas pipeline connecting Turkey with the Azerbaijani exclave of Nakhchivan will subsequently be expanded to Europe. This move has been envisioned as part of a wider central Asian, or ‘Turkic’, trade corridor, to advance the economic integration of the region, with Turkey as the key transit point in this wider Eurasian machinery.

Nevertheless, conflicts in Nagorno-Qarabag and in Ukraine pose considerable challenges for proponents of this grand vision. The Azerbaijani government appears intent on subsuming the issue of natural gas, and the Nakhchivan fields, into its ongoing negotiations with Armenia. This shifts the discussion from one concerning a wider Eurasian system, to a narrower regional arrangement.

Despite the fraught politics of the region, geopolitical and strategic factors suggest the role of Turkey as a trans-shipment and trans-loading hub will grow in importance over the coming years. Even as the EU intends to break down its reliance on Russian raw materials, CRMs, mined and processed in central Asia and Africa, will be required to meet increasing demand in the EU. The most direct route from central Asia to the EU passes through Turkey. Meanwhile, the major African export hubs – Djibouti and Suez – are concentrated in the east of the continent positioning the Eastern Mediterranean, with Turkey at its heart, as the most natural through-route to Europe.

As the conflict over Nagorno-Qarabag is resolved, it appears likely that plans for connecting pipelines through the Caucasus to Europe will be revived. There is currently no cheaper, geopolitically more expedient route for the west to pursue in its mission to shed reliance on Russian gas, than the Turkey-Azerbaijan route, which connects with rich supplies of Gulf Arabian oil and gas. These dynamics mean the prospect of a wider energy system integrating central Asia and the Middle East – through Turkey – to Europe is likely mid-term. This will foster economic integration and interdependence, enabling the energy corridor to function also as an artery of trade. This dynamic will undoubtedly increase the importance of Turkey as a transit hub for commercial goods.

Such an outlook carries some general implications for governments in their approach to the trans-shipment economy, and to Turkey specifically. Governments should thus be guided, in their approach to the region, by several important factors.

Implications for governments:

- Historical Importance: Turkey, especially during the Ottoman Empire, played a crucial role in connecting global trade, acting as a bridge for goods and commodities between Europe and Asia. This historical position highlights Turkey’s potential to regain its status as a key transit hub.

- Economic Growth: Turkey’s economic policies, particularly its move towards liberalization and openness to imports, have contributed to its growth and re-emergence as a trans-shipment hub. This has important implications for Turkey’s economic development and stability.

- Foreign Direct Investment: The country’s attractiveness for foreign direct investment and the booming industry for cheap electrical appliances have had a positive impact on Turkey’s exports. This suggests potential opportunities for foreign investors and businesses.

- Diplomatic Sensitivity: Turkey’s geographical location places it at the crossroads of major geopolitical zones, including the EU, Russia, the Middle East, and the Eastern Mediterranean. Its diplomatic approach of maintaining close ties with regional players while acting as a bridge has implications for its role in international diplomacy and trade relations.

- Russia Relations: Turkey’s refusal to follow Western sanctions on Russia during the Russo-Ukrainian War and its role as a conduit for Russian goods into the EU highlight its ability to influence international trade dynamics. This underscores the need for careful diplomatic navigation in such situations.

- Energy Hub: Turkey’s potential role as an energy hub, especially in the wake of the Russo-Ukrainian War, is expected to boost its transit economy. This could have significant implications for energy supply routes and the economic integration of the region.

- EU Reliance: The EU’s dependence on Turkish transit for raw materials, like copper, from Russia has led to a unique trade dynamic. This reliance on Turkey for transit trade underscores the importance of its role in the global supply chain.

- Regional Conflicts: Conflicts in regions such as Nagorno-Qarabag and Ukraine can impact plans for trade corridors and transit routes. Governments and firms should consider these conflicts when planning trade and transit strategies.

- Long-Term Transit Trade: The concentration of major African exit ports for the EU in the Eastern Mediterranean and Turkey’s strategic location as a connecting corridor for central Asia to the EU make it a crucial player in the long-term transit trade. This has implications for governments and businesses engaged in international trade.

Implications for firms:

Transport, logistics, and shipping firms in the region have an opportunity to benefit from Turkey’s re-emergence as a transit hub. However, they should also be aware of the potential risks and challenges associated with operating in a geopolitically sensitive region.

- Opportunities for Growth: The re-emergence of Turkey as a trans-shipment and trans-loading hub presents significant growth opportunities. Firms can benefit from the increased demand for their services, including shipping, warehousing, and logistics.

- Strategic Investment: Firms may consider strategic investments in expanding and upgrading their facilities and infrastructure in Turkey. This is particularly relevant for companies involved in container handling, storage, and port operations.

- Diversification of Services: To meet the needs of the evolving trade routes, firms can diversify their services. This might include offering intermodal transportation options, better connectivity with major shipping routes, and efficient trans-loading services.

- Collaboration and Partnerships: Collaborating with Turkish authorities and port operators can lead to mutually beneficial partnerships. Joint ventures or agreements with local entities can enhance efficiency and access to key trans-shipment locations.

- Risk Management: Given Turkey’s geopolitical sensitivity and its role in international diplomacy, firms should engage in robust risk management strategies. This includes contingency plans for any disruptions due to regional conflicts or diplomatic tensions.

- Market Positioning: Firms should position themselves strategically to cater to the growing demand for trans-shipment services. This may involve marketing efforts and the development of specialized solutions for the transit trade.

- Energy Sector Expansion: Companies involved in energy transport, such as those handling natural gas, should monitor developments in the energy sector. The expansion of Turkey as an energy hub could create new opportunities for these firms.

- Long-Term Planning: Consider the long-term impact of Turkey’s role as a transit hub. It’s likely to remain crucial for commercial goods transit, so long-term planning should be aligned with these expectations.

___________________________________________________

1Statistics estimated using the following sources: Giovanni-Tena World Trade Historical Database (2018) Federico, G. and Tena-Junguito A. (2019): World trade, 1800-1938: a new synthesis. Revista de Historia Económica-Journal of Iberian and Latin America Economic History, Vol 37, n.1.; Ortiz-Ospina, E. et al. (2018) ‘Trade and Globalization’. Our World in Data.

2The mean percentage of transshipment per total exports in 1890 across 66 polities studied is estimated at 7.54%.

3 1913 borders are used for the Ottoman Empire, which exclude its former Balkan possessions and Egypt. Meanwhile Lebanon, Syria and the Arabian Peninsula are also omitted, to provide the closest possible geographical analogy to modern Turkey.